Company information

N26’s mobile app puts the control in your hands with real-time banking: categorize your spending, send money to friends, save and budget your money, enable/disable foreign payments, transfer money in 19 currencies, set payment limits, lock your card and more – all from the comfort of your phone.

N26, founded in 2013 in Berlin, is Europe’s first mobile bank. Its founders shared a vision of building a bank people would actually love using, fitting seamlessly into their mobile lifestyle. In 2015, N26 officially launched its online banking app, offering more transparency, flexibility, and control for the customer, and eliminating the interference and physical boundaries too-often characterized by a traditional bank.

Opening an account with N26 is easy and quick – all you need is proof of ID, an email address and a mailing address (to receive your Mastercard).

To date, over 2.5 million customers from 24 different European countries use N26, with a US launch planned for 2019.

Cards

What I Like About N26

N26 offers several compelling advantages that have kept me satisfied with my choice:

No ATM Withdrawal Fees: With N26, I can enjoy three free ATM withdrawals each month, a feature that has saved me a significant amount of money. It’s a stark contrast to the 5-7€ charges imposed by most German banks for using other bank’s ATMs. With N26, I’ve been able to withdraw cash without worrying about fees for years, even from the less reputable ATMs found in late-night shops and train stations.

No Monthly Fees: Unlike many other banks that have introduced monthly fees, N26 still offers a free plan. This was a major reason I initially opened my account in 2016. I firmly believe that access to a bank account should not come with a recurring cost.

Available in English: N26’s commitment to offering its services entirely in English has been incredibly valuable to me. Their app, website, and customer support are all accessible in English, making banking in Germany far more accessible for non-German speakers.

Fully Digital: N26’s online platform allows you to perform all banking tasks without ever needing to visit a physical bank branch or deal with paper mail. This convenience is particularly advantageous for those who frequently travel or prefer the ease of online banking.

Competitive Exchange Rates: N26’s MasterCard is an excellent choice for travelers like myself. It offers favorable exchange rates, with no transaction or currency conversion fees, except when withdrawing cash in foreign currencies. For frequent travelers, N26 You and N26 Metal accounts offer unlimited ATM withdrawals in all currencies, along with travel insurance.

Transaction Notifications: One of my favorite features is receiving instant notifications on my phone for every transaction. This has not only helped me stay vigilant about my spending but also allowed me to quickly identify any unexpected activity.

No Anmeldung Required: N26 simplifies the account-opening process by not requiring a registration certificate (Anmeldebestätigung) to open an account. This flexibility is particularly helpful for those who have recently moved to Germany and may not yet have a permanent address.

Support in English: N26 is unique in offering full English-language support, a rarity among German banks. The app is available in five languages: English, Spanish, French, Italian, and German.

Quick and Easy Signup: Opening an N26 account typically takes just 10 minutes, and it can be done from anywhere globally, provided you have a phone with a camera. While the registration process isn’t always flawless, it can be exceptionally swift when everything goes smoothly. You’ll receive your bank card within a few days.

Exploring Other Options: While N26 has served me well, it’s always prudent to explore other banking choices to find the one that aligns best with your needs. ING and DKB are strong alternatives, especially for those who prioritize fee-free ATM access. For non-German speakers, bunq is another worthy consideration.

Areas for Improvement

Despite its many strengths, N26 is not without its drawbacks:

Deteriorating Features: Over time, N26 has introduced fees and limitations that were not present initially. These changes include fees for plastic MasterCards and a reduction in the number of free ATM withdrawals. Unfortunately, this trend of banks imposing more fees is not unique to N26 and affects many financial institutions.

Limited Free ATM Withdrawals: The free N26 account allows only three free ATM withdrawals per month, which may not be sufficient for some individuals, particularly in a cash-driven country like Germany. Older accounts still enjoy five free withdrawals each month, which offers more flexibility. If you require more frequent ATM access, DKB and ING are preferable options.

Account Creation Issues: Although the N26 account opening process typically takes only 10 minutes, some users have reported difficulties during ID verification, resulting in delays in receiving their bank cards. This is something to consider if you need a bank account urgently.

Two-Factor Authentication Dependency: N26’s reliance on two-factor authentication via a mobile phone means that losing access to your phone can lead to issues accessing your bank account. Unlike banks with local branches, N26 lacks alternative methods for accessing your account if your phone is lost or stolen.

Coin Handling Challenges: Depositing coins can be cumbersome with N26, as CASH26 is not suitable for substantial coin deposits. Eventually, you’ll need to exchange your coins at the Bundesbank, which, while not a major issue, can be inconvenient. Traditional banks like Commerzbank and Deutsche Bank offer more straightforward coin deposit options.

Limited Services: While N26 excels in everyday banking, it does not offer extensive investment options or specialized services like mortgages. For these needs, traditional banks such as Commerzbank or Deutsche Bank may be more suitable.

Slow Customer Support: N26’s customer support, while available in English, has received criticism for its slow response times. Many users have reported delays in receiving assistance, which requires patience.

App Bugs (Mostly Resolved): The N26 app has experienced occasional bugs in the past, including issues with transaction approvals. Although most of these issues have been resolved, it’s advisable to stay vigilant and updated.

Is N26 Safe?

Yes, N26 is a secure banking option. It is an established bank with thousands of employees and is backed by government deposit insurance of up to 100,000€. Your funds are well protected.

Banking Features

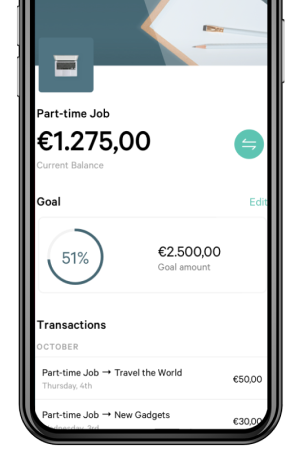

Spaces

Create sub-accounts to separate your money for different budgeting goals (e.g. savings, mortgage payments, holidays etc.). You can add, remove or move money between your spaces. Spaces are great for saving as the money can’t be used for spending.

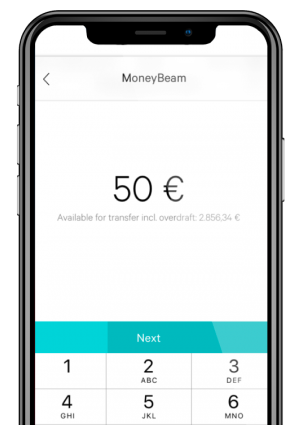

MoneyBeam

With MoneyBeam, users can send money to contacts in their phone’s contact list without the need for bank details. N26 users will receive the money instantly; others get a link with which they can collect transfer within 2 banking days.

Pros

- Fee-Free ATM Withdrawals: N26 offers 3 free monthly ATM withdrawals, saving you money on access to your cash.

- No Monthly Charges: Unlike many banks, N26 provides a free account option, eliminating monthly fees.

- English Support: N26’s app, site, and customer service are in English, easing accessibility.

- Online Banking: Manage your finances entirely online, no need for physical branches.

- Competitive Exchange Rates: N26 provides favorable rates for international transactions, great for travelers.

- Instant Transaction Alerts: Receive immediate notifications for all financial activities, aiding spending control and fraud detection.

- No Anmeldung Needed: N26 doesn’t demand a registration certificate, making it newcomer-friendly.

- Swift Account Opening: You can open an N26 account in about 10 minutes via smartphone and receive your card promptly.

Cons

- Reduced Features Over Time: N26 introduced fees and limitations, diminishing long-term benefits.

- Limited Free ATM Withdrawals: Free withdrawals are capped; exceeding incurs fees.

- Account Creation Challenges: Some users face verification delays and post office visits for identity validation.

- Two-Factor Authentication Dependency: Access hinges on mobile two-factor authentication, risky if the phone is lost.

- Coin Deposits Difficulty: Large coin deposits are challenging; users must exchange coins periodically.

- Limited Services: N26 primarily suits daily banking, lacking advanced investment, credit, and mortgage options.

- Slow Customer Support: Complaints about sluggish customer support response times persist.

- Incomplete Translations: Some app parts may remain in German, despite overall English availability.